Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1310.5 | -16.3 | -1.23% |

| Eurostoxx Index | 2135.2 | -51.6 | -2.36% |

| Oil (WTI) | 78.44 | -1.3 | -1.65% |

| LIBOR | 0.461 | -0.001 | -0.22% |

| US Dollar Index (DXY) | 82.51 | 0.250 | 0.30% |

| 10 Year Govt Bond Yield | 1.62% | -0.06% | |

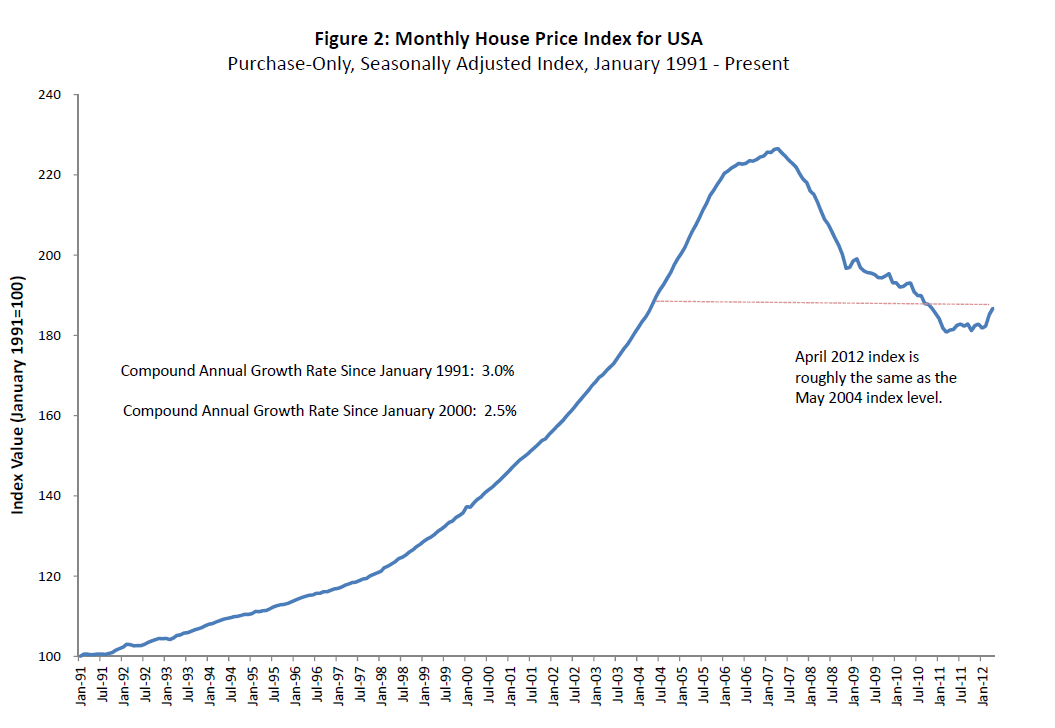

| RPX Composite Real Estate Index | 181.4 | 0.2 |

A soggy tape to match a soggy morning here on Wall Street. There is no real news driving futures down, just a sense of malaise coming out of watching the European slow-motion train wreck. Euro sovereigns are slightly wider, while the US 10-year is up about a point. MBS are higher as well.

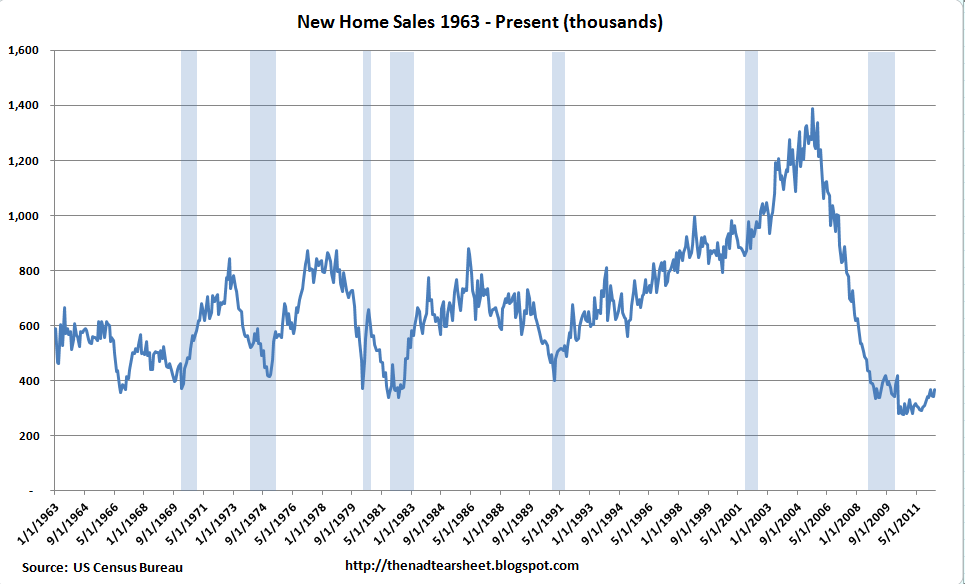

New Home Sales came in at 369k, well ahead of expectations of 347k. That said, we are still running at levels below the bottoms of recessions going back to the 1960s and well below the average 700k pace from 1963 to the bubble burst.

We have a lot of economic data this week, with April Case-Schiller and Consumer Confidence coming out tomorrow, Durable Goods and pending home sales Wed, Initial jobless claims and final Q1 GDP numbers on Thurs, and Personal Income / Spending numbers on Fri. We also have a European summit (something like #18) and will potentially hear the fate of Obamacare as well.

We are in earnings pre-announcement season, where companies who are going to miss their quarters disclose it to the market. Earnings season will officially begin in two weeks with Alcoa’s numbers.

Treasury yields will hit 1% by year end, says CNBC. Certainly that is a possibility if nothing is done about Taxmageddon or if Europe implodes. Simon Johnson is worried about how US banks will handle a European implosion, and even introduces a new risk we can wring our hands over: Dissolution Risk.

The Chicago Fed National Activity Index declined to -.45 in May from +.08 in April, which indicates slowing economic growth. Positive numbers indicate the economy is growing above trend, while negative numbers indicate the economy is growing below trend. The 3 month moving average, decreased to -.34 from -.13 in May. If the 3 month moving average falls below -.7, it typically means a recession has already begun.

$9.3 billion. That is the amount of money people lose per year responding to those ubiquitous Nigerian email scams. To put that number in perspective, that is roughly what GM made last year and accounts for 11% of Nigeria’s GDP.

Filed under: Morning Report | 16 Comments »