Stocks are flat this morning as the FOMC begins their two day meeting. Bonds and MBS are up small after getting whacked yesterday.

Mortgage applications fell 7% last week, as purchases fell 4.2% and refis fell 9.1%.

The NAHB Homebuilder index hit a post-recession record of 62 – the highest since October 2005.

The consumer price index fell 0.1% month-over-month as the strong dollar hurts commodity prices. Ex-food and energy, prices were up 0.1% month-over-month and 1.8% year-over-year. That is close to the Fed’s target, however they prefer to use the personal consumption expenditures data, which uses a different balance of goods to calcluate it.

Real average weekly earnings rose 2.3% last week.

When the FOMC releases their decision tomorrow, they will include their economic forecasts. For this entire recovery, the Fed’s estimates of future growth have been consistently high. IMO, the reason for this comes from the fact that the Fed’s models are largely based on prior experience which has been Fed-driven inventory-based recessions since WWII. In these cases, inflation increases -> the Fed raises rates -> the economy slows -> inventory builds up -> people get laid off -> a recession begins -> the inventory gets sold -> new production starts up -> workers get re-hired -> the economy recovers. These recessions are typically short and the recoveries tend to be V-shaped. This recession is different because it wasn’t driven by the Fed raising rates and inventory buildup, it was driven by a bursting asset bubble. The issue with these recessions is that the problem isn’t excess inventory – it is bad debt and mal-investments. And these are typically longer and deeper recessions, with longer and shallower recoveries. Instead of a V-shaped recovery, you get a bathtub-shaped recovery. The economy recovers once the bad debt and bad assets are liquidated, which takes longer.

This leads into the latest negative equity report by CoreLogic. 10.9% of all homes with a mortgage (or about 5.4 million homes) have negative equity. 9 million (or about 18%) have a small amount of equity. 800k homes with negative equity would become equity positive if house prices increase 5%. Note that many of these properties may never sell (abandoned homes in rust-belt cities for example) so the effect on the real estate market will probably be muted. But that is one of the reasons why the inventory of existing homes for sale is so small. Negative equity has a drag on the economy be preventing workers from moving to where the jobs are because they cannot sell their house without a ding on their credit ratings. Just another example of the mal-investments that hold back the economy. The economy will accelerate as these mal-investments are liquidated and borrowers and creditors move on.

Stocks are up this morning as we await the big day Thursday. Bonds and MBS are down.

Retail Sales rose 0.2% in August, just missing the 0.3% Street estimate. The control group (which excludes volatile and price-sensitive goods like autos, gasoline and building supplies) rose 0.4%, which was better than the 0.3% Street estimate. August is the back-to-school month, so overall decent numbers, which bodes well for the holiday shopping season. Big retailers like Amazon.com and Wal Mart are up pre-open.

Industrial Production fell in August by 0.4%, which was lower than the -0.2% estimate. Capacity Utilization fell to 77.6% from 77.8%. Separately, the Empire Manufacturing Survey (which measures manufacturing activity in New York State) was highly negative at -14.7. The strong dollar is taking a bite out of manufacturing activity.

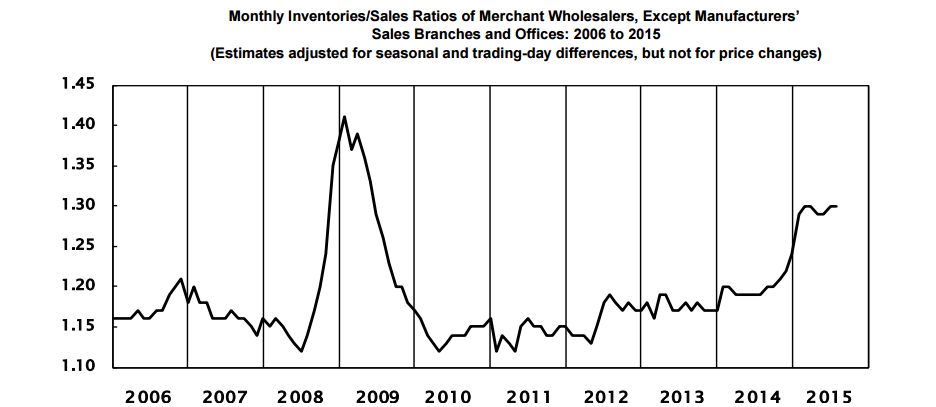

Business inventories and sales rose 0.1%. The inventory-to-sales ratio held steady at 1.36x. The inventory / sales ratio has been ticking up recently, which is a worrisome sign, at least for a cyclical recession. During recessions, it is not uncommon to see a big spike in this ratio. Historically, it has been much higher. You can see on the graph below the latest increase, and also the secular decline in the ratio that began in the mid-80s as manufacturing implemented just in time inventory management.

Tim Duy, an influential Fed-watcher makes the case for not moving this week. His argument: With rates at the zero bound and market turmoil, the Fed has no margin for error since it is more or less out of ammo. Better to wait until the waters are calmer to make a move. FWIW, I tend to agree with those arguments, and I think the Fed is very wary of a 1937 scenario. Inflation is nowhere to be found and while there is a bubble in credit markets, widening credit spreads are acting as a tightening all by themselves (the Larry Summers argument).

The argument for raising rates: – we have bubbles in the credit markets, and certainly in the pre-IPO market. Uber, which earns nothing, and has a market cap similar to Dow Chemical, is indicative of a craziness we haven’t seen since the skyrocketing IPOs of eToys and Pets.com in the late 90s. Stocks are up 200% from the lows in 2009. His point is that we DO have inflation – but it is “too much money chasing too few assets,” not “too much money chasing too few goods.” Imagine if the Fed had raised rates in 2003 and the real estate bubble had popped in 2004. We still would have had a recession, but I seriously doubt the banking system would have collapsed the way it did in 2008. And the recession would have certainly been shorter and less severe than 2008 – 2009. His point: it is time to end the addiction to low interest rates. The economy is strong enough to take a Fed Funds rate of 50 basis points. This argument is highly, highly unpopular in policy circles, so it won’t get any traction. The consensus in Washington (at least on the left, which runs things at the moment) was that policy had absolutely nothing to do with the bubble – it was 100% Wall Street Sharpies that did it, and “smart regulation” will prevent another one from happening.

Note that the one advocating for standing pat is a professor, and the one advocating moving is a trader. So they will look at the issue from two entirely different points of view.

As credit spreads have widened, we have seen some jumbo securitizations pile up at the banks. This probably signals less aggressive jumbo pricing ahead. LOs – something to tell your borrowers, especially if they are thinking of floating right now. Even if the 10 year bond goes nowhere, jumbo rates could be heading up.

Markets are flattish this morning as overseas markets stabilize. Bonds and MBS are up.

No economic data today. We will have some important economic data this week retail sales and industrial production on Tuesday, with housing starts on Wednesday.

The big event this week will be the FOMC meeting on Wednesday and Thursday. The announcement will come on Thursday. For mortgage bankers, the focus will be in the Fed Funds rate, and also “reinvestment tapering.” Reinvestment tapering has to do with the Fed’s re-investment of maturing Treasuries and MBS that it bought during QE. Currently, the proceeds from any maturing MBS are re-invested back into the MBS market, in order to keep the Fed’s balance sheet constant. At some point, they will stop doing that, and you may see mortgage spreads widen. This means that mortgage rates could increase, even if the 10 year goes nowhere. Note that they probably will taper, meaning they won’t stop re-investing maturing proceeds all at once. They’ll probably cut it by $5 billion a month, similar to how they executed the tapering in the first place.

The Fed Funds futures are currently projecting about a 30% chance the Fed will tighten this week. Fed Vice Chairman Stanley Fischer is advocating moving before the inflation numbers begin to rise. “There is always uncertainty and we just have to recognize it,” he told CNBC television on Aug. 28. Asked if the Fed should delay an increase until it had an “unimpeachable case” that a move was warranted, Fischer replied, “If you wait that long, you will be waiting too long.” On the other side of the coin, many in the Fed are worried about repeating the mistake of 1937, where the Fed tightened (really only by a little bit) and the economy dove back into recession.

Exhibit (A) in the “ZIRP is not free” argument: Petrobras sold 100 year (!) bonds last June, and as oil has dropped so have these bonds. They dropped into the 60s recently. What does this have to do with ZIRP? Everything. When central banks hold down rates artificially, the price signals the market uses to assign risk (interest rates) become distorted and investors are forced to reach for yield. You see it mainly with pension funds and insurance companies, which have to hit a return bogey based on longevity and health care inflation. Yes, getting 6.85% in this interest rate environment is attractive, but, you are lending to a Brazilian oil producer for 100 years and only getting 6.85% a year! The last 3 times the Fed raised rates (94,99, and 05) they blew up the MBS market, the stock market bubble and the residential real estate bubble. This bond issue shows how much of a credit bubble we currently have. The Fed may have painted themselves into a corner, but until inflation comes back, they can wait.

Presidential candidates are beginning to put out their tax and spending plans. Jeb Bush recently put out his tax plan, and there are some items that will directly affect those in the real estate business. First, his plan reduces rates and limits deductions. State and local taxes will no longer be deductible. Second, there will be a cap on itemized deductions, which means people who have a large mortgage and pay a lot of mortgage interest will find themselves with a higher tax bill. This will probably have a negative effect on the jumbo side of the market, although it will present an opportunity for LOs to try and pitch refinancing from 30 year mortgages to 15 year mortgages. While the mortgage interest deduction is as American as apple pie and may in fact be a political third rail, economists believe that it hasn’t really increased the homeownership percentage, as it was intended to do – it just encouraged people to buy bigger houses.

I was on the trading floor at Bear, Stearns in London. It was just after lunch. A headline went across Bloomberg saying a plane had hit one of the WTC towers. CNBC mentioned the story as well, but no one was thinking “terrorism.” I emailed one of my friends at Merrill Lynch (right across the street at the World Financial Center) and he wasn’t even aware of what happened. The European markets were down a bit on the day, but didn’t really react to the first hit.

After a few minutes, CNBC started showing live footage of the fire and then we saw plane 2 hit. Immediately, the world realized what had happened. The Euro markets were collapsing and I was inundated with sell orders. The news of the Pentagon hit came out. People on our floor started freaking out. We were in Canary Wharf (One Canada Square) in the tallest building in the UK. Planes routinely come close to the building as they approach City Airport. The head of Bear Stearns Europe came on the trading floor and told everyone if they were uncomfortable, to go home. No one knew if today was “fly a plane into financial headquarters day” Everyone bailed, and I was one of the last guys on the trading floor, trying to reconcile my book by hand and get flat before I left.

I looked up at CNBC before I left and saw the place I got married at a year earlier collapse on my birthday.

P.S. As I headed to the tube to go home, I passed the Slug and Lettuce (a pub) and found all of the “uncomfortable” Bear Stearns employees having a pint directly below the building they were so uncomfortable being in.

Stocks are lower this morning as emerging markets fall. Bonds and MBS are flat. Overnight, China intervened in the f/x markets to support the yuan. China’s surprise devaluation in August was the catalyst for this whole sell-off.

Remember, when you read the words “Chinese supporting the yuan” think one thing: Treasury sales and increasing interest rate. The Chinese support the yuan by selling dollars, and the way they sell dollars is by selling Treasuries.

Brazil was downgraded to junk by S&P yesterday. This is part of the reason why emerging markets are heavy this morning. This move was expected eventually, however the speed in which it happened was surprising. Does this put a bid under Treasuries? Nope.

Import prices fell 1.8% in August and are down 11.4% year over year. A strong dollar is depressing commodity prices and making imports more cost competitive.

Initial Jobless Claims came in at 275k, a drop from 281k the week before. People who have jobs are generally keeping them.

The Bloomberg Consumer Comfort Index was flat at 41.4 last week. 2/3 have a negative view of the economy. while 55% have a positive view of their own personal financial situation.

Wholesale inventories fell 0.1% in July, while wholesale sales fell 0.3%. The inventory to sales ratio, which can be considered a leading indicator for a recession is at 1.3x, an elevated reading. This would signal a recession is a possibility.

The current continuing resolution to keep the government open expires at the end of the month. Government shutdown talk will undoubtedly escalate as the two sides posture over funding Planned Parenthood.

To its proponents, Keynsianism cannot fail, it can only be failed. Dr. Cowbell is worried that Abenomics will fail in Japan. Of course Japan has followed the Keynsian playbook to the letter for 25 years and has had no growth and a debt to gdp ratio of 2.2x to show for it. Whenever you hear people saying: we need to spend big on infrastructure to put people to work and get the economy going again, remember they are basically putting the old New Deal / Japanese wine in a new bottle.

Stocks are higher this morning on overseas strength in equity markets led by Japan. Bonds and MBS are down.

Mortgage Applications fell 6.2% last week, with purchases falling 0.9% and refis falling 9.9%.

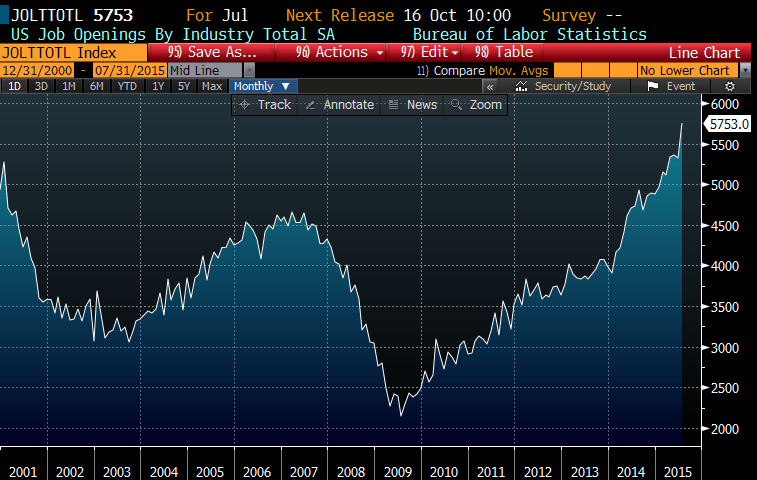

Job openings hit a record in July, with the JOLTS job openings hitting 5.7 million. Compare that number with the number of unemployed at 8 million. The quits rate (which is a measure of economic strength) has been unchanged for the past year however at between 2.7 million and 2.8 million. It seems surprising to see a labor force participation rate at 38 year lows, job openings at highs, an unemployment rate at boom time levels, and almost no real wage growth. It speaks to a mismatch between what business wants and who is available.

Chart: JOLTS job openings:

Citi is forecasting a better than 50% chance of a global recession in the next couple of years. This will be led by emerging markets and China. While that doesn’t necessarily mean the US will head into a recession, it does mean that there will be little to no upward pressure on interest rates. The biggest risk to the US is a sharp increase in the US dollar, which will hurt exporters. The policy response to a recession will be limited – monetary policy is already at pretty much full stimulus. Much more worrisome however, is the fact that protectionist policies are gaining in popularity.

Homebuilder Hovnanian reported earnings this morning. Deliveries fell 3.8% compared with last year. Gross margins were down as well. Contracts did expand however, to almost 20%. It seems like the builders in general had a bit of a lull in deliveries over the summer, but almost all reported bit increases in contracts and backlog. We are entering the slow season for the builders, which lasts about as long as football season. While I sometimes feel like Linus in the pumpkin patch, 2016 could be a big year for the builders. Would be nice to get housing starts back around historical levels of 1.5 million or so.

Larry Summers is out with another editorial which lays out the case for keeping rates at zero. His argument is that credit spreads have widened (which means the interest rate companies have to pay to borrow) has increased over the past month and that in of itself constitutes a tightening. David Stockman (Reagan’s budget director) was on Bloomberg Radio this morning excoriating the “clowns at the Fed” for not having raised rates already. His point is that the unemployment rate is in the middle of the range of what the Fed considers full employment. In fact, the 5.1% unemployment rate is in the bottom quintile of unemployment rates over the past 40 years.

Stocks are higher this morning on overseas strength. Bonds and MBS are down.

The Labor Market Conditions Index rose 2.1% in August, better than the forecast. This is an index of various leading and lagging indicators.

The jobs report last week probably didn’t move the needle one way or the other with respect to the Fed’s decision next week. Yes, payrolls disappointed, but the 2 month revision was strong. The labor force participation rate remained mired at 38 year lows, however the unemployment rate ticked down and wage inflation ticked up ever so slightly. Note that August’s payroll miss seems to have a seasonal element to it and is usually revised upward.

The bond market seems to be ready for a rate hike. The Fed Funds futures are forecasting a very slow pace of tightening, the yield curve remains positively sloped, with the 10 year bond relatively heavy. Option volatility shows little sign of panic. The 10 year bond forward contracts indicate that even if the Fed hikes rates, the 10 year should maintain levels right around here.

The NFIB Small Business Optimism index edged up in August. Note that the survey was taken before the sell-off of the last few weeks. The labor data was decent – with businesses adding 0.13 workers, a historically strong number. Interestingly, 56% reported hiring or trying to hire, however 86% of those who are trying to hire are unable to find qualified candidates. (I wonder if “qualified” means someone with the wisdom of a 60 year old, the vision of a 50 year old, the efficiency of a 40 year old, the drive of a 30 year old and the paycheck of a 20 year old). Note that obama made an executive order over the weekend demanding that Federal contractors offer paid sick leave.

Completed foreclosures dropped to 38,000 in July, according to CoreLogic. This is down 24% from last year, and 6% from June. Pre-financial crisis, 21,000 was a typical reading, so we have a way’s to go yet. Foreclosure filings have ticked up this year as the judicial states start to address their foreclosure inventory. The Northeast and Florida remain the states with the highest foreclosure inventory.

Stocks are higher this morning after Chinese markets rallied to almost unchanged after an early swoon. Bonds and MBS are down.

Mortgage Applications rose 11.3% last week as purchases rose 4.1% and refis rose 16.8%. The 30 year fixed rate mortgage was steady at 4.08%. While the bond market has been pretty volatile, TBAs have been much more steady, tending to fade the moves of the bond market. This means you might see a big drop in the 10 year yield, hope to lock at a great rate, only to find that rates are lower, but not as much as the big move in Treasuries would suggest.

The ADP jobs report showed payrolls increasing by 190,000 jobs, which is less than forecast. July was revised lower as well. The Street is forecasting an increase of 218,000 in the official report on Friday.

After a couple big quarters, unit labor costs fell in the second quarter by 1.4%. This number tends to be volatile, as does productivity. The Fed pays close attention to these numbers.

The ISM New York Index fell pretty dramatically in August, from 68.8 to 51.1. The 68.8 reading was unusually good, while the 51.1 reading was unusually bad.

Factory orders rose 0.4% in July, lower than the 0.9% forecast. Ex-transportation, factory orders fell 0.6%.

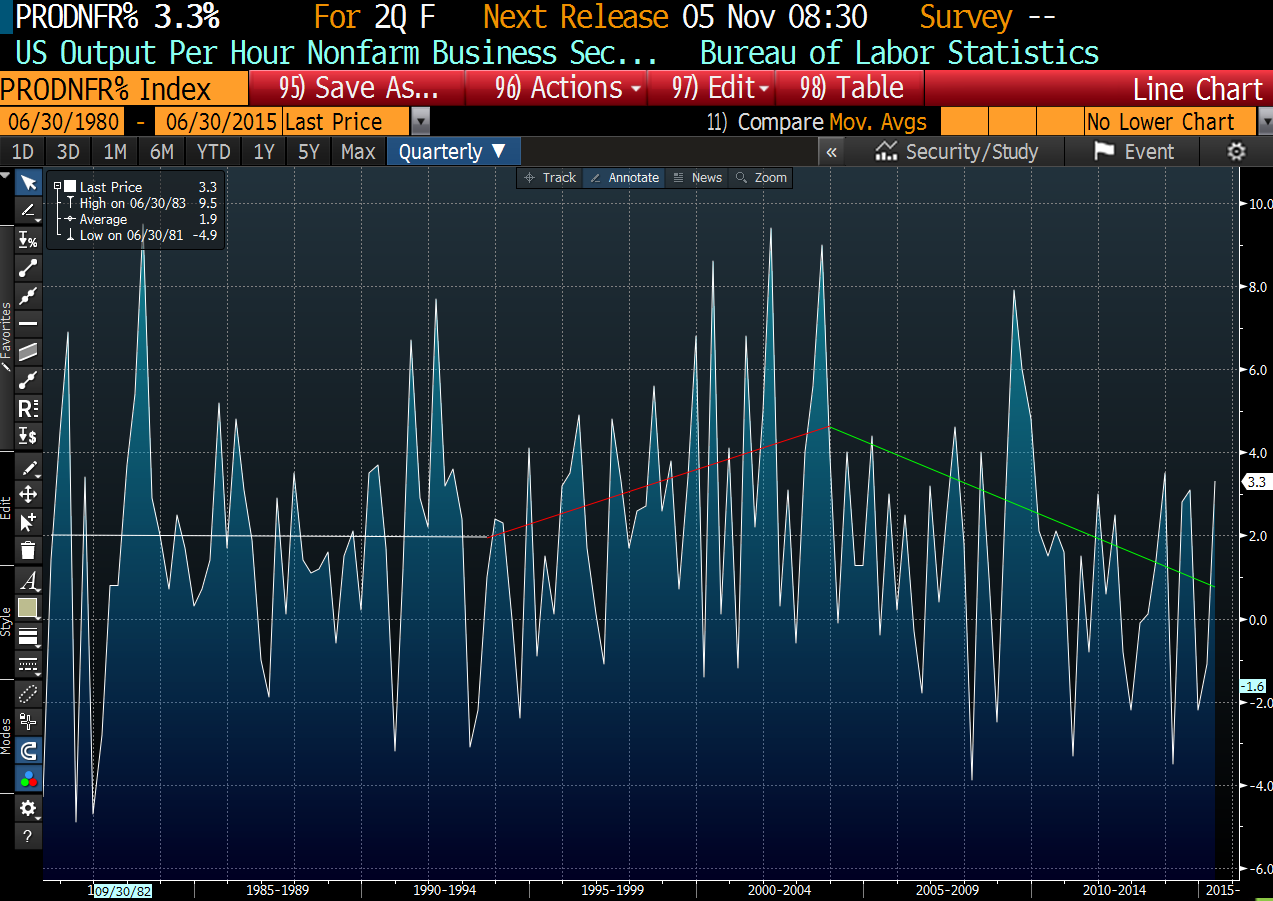

Productivity rebounded in the second quarter to an annualized rate of 3.3%. Overall, productivity growth has been in a downtrend for the past dozen years or so. This is one reason why wage inflation has been so hard to come by – productivity growth has been declining. Take a look at the chart below. You can see productivity flatlining around 2% in the 1980s, then a big acceleration in the 1990s as the personal computer goes from a glorified typewriter to an indispensible tool on everyone’s desk. That continues into the early 00s as the internet helps business become more productive. Finally, you see the decline as the PC and Internet phenomenons become played out. While the mainstream media mocked Jeb Bush for talking up the importance of productivity, he was right.

Is “quantitative tightening” the new buzzword? Not yet, but as central banks worldwide begin to let go of some of their reserves, it may become more common. For the past two decades, central banks (especially China) have been accumulating reserves as they manage their trade balances and their currencies. The net effect has been a bid under Treasuries and a release of money into the system. As China slows, this is reversing as they sell Treasuries to support their currency. When they sell Treasuries, they put pressure on US interest rates and the withdrawal of liquidity acts like a tightening. Punch line: this is the second-order effect of the global slowdown – you might see upward pressure on interest rates, a rising dollar, and a withdrawal of liquidity. This would compound the effect of any Fed tightening. Which means a bumpier road ahead as the Fed pursues normalization. This might explain why the Fed has chosen to not sell (and even to keep re-investing) its portfolio of Treasuries and MBS that it bought during QE.

As world markets recover from last week’s bloodbath, the probability of as Sep rate hike is increasing.

Stocks are lower this morning on global growth fears. Bonds and MBS are up.

IMF Managing Director Christine Lagarde said that global growth will likely remain weaker than the IMF was projecting two months ago. Chinese manufacturing fell to a 3 year low.

China continues to sell US Treasuries in order to support its currency. There has been a fear that China could take down the US by dumping Treasuries and pushing up interest rates here. In reality, the US has more leverage here. China’s economy is beginning to soften, and the last thing they would want to do is injure their biggest customer. Second, Japan would gladly take China’s supply of Treasuries. Third, the article mentions that China has no better alternatives than US Treasuries to stash a trillion dollars. Actually I think that is wrong. The proceeds will go to pay off domestic debt pledged against falling asset prices within China.

The ISM Manufacturing Survey fell to 51.5 in August, missing the Street expectation of 52.5. Prices paid fell from 44 to 39.

Economic Optimism took a big hit in August as well, as the index fell from 46.9 to 42, missing the Street expectation of 47.1 by a country mile.

Constructions spending rose 0.7% in July and June was revised upward from 0.1% to 0.7%.

Obama threw a bone to organized labor as his National Labor Relations Board ruled that companies that use contractors are considered joint employers. This makes parent companies liable for how their subcontractors treat their employees and also is intended to make it easier for unions to get a foothold in the big fast food chains. Who else has to worry about this? The homebuilding industry, which uses a lot of contract labor and has since the 1980s. “Are we concerned that this ruling might have some impact? I think we are alert to the ruling. We are aware that the Labor Department feels its mandate is broad, but we think that our business is highly differentiated from what’s being discussed in the current case or even extensions,” said Stuart Miller, CEO of Miami-based Lennar. Given how much homebuilding means to the overall economy, depressing the sector even further is not really what the economy needs at the moment. And the lack of housing supply leads to…