Vital Statistics:

| Last | Change | Percent | |

| S&P Futures | 1354.8 | -3.7 | -0.27% |

| Eurostoxx Index | 2257.6 | 6.9 | 0.31% |

| Oil (WTI) | 88.99 | -0.2 | -0.26% |

| LIBOR | 0.455 | 0.000 | 0.00% |

| US Dollar Index (DXY) | 83.24 | 0.210 | 0.25% |

| 10 Year Govt Bond Yield | 1.48% | -0.03% | |

| RPX Composite Real Estate Index | 184.5 | 0.4 |

Markets are a little weaker on no real news. A slew of banks reported earnings this morning, and most were better than expected. Bond yields are back below 1.5% and MBS are up slightly. The Bernank’s testimony continues today.

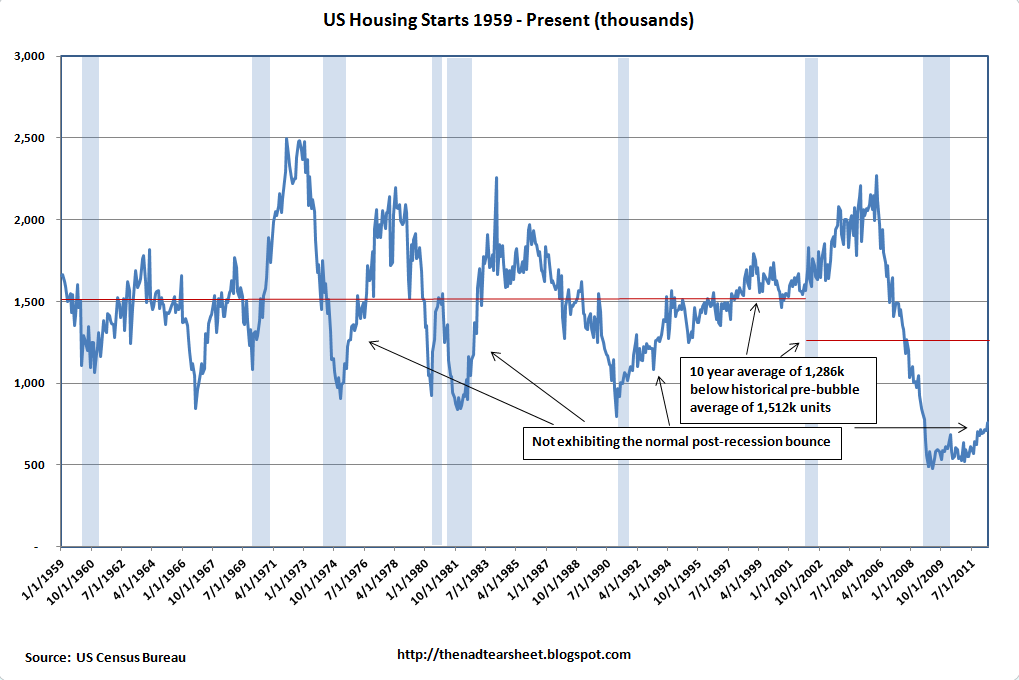

Housing starts came in at 760k in June, an increase from a revised 711k in May. While most other sectors in the economy are decelerating, the housing construction sector is accelerating. That said, housing starts are a long way from normalcy. Sentiment in the homebuilders has been improving as well, with the NAHB Builder Confidence Index rising smartly in July.

Housing Starts:

NAHB Housing Index

On the heels of San Bernardino’s eminent domain proposal, Georgetown Professor of Law lays out another avenue to deal with underwater equity – “quasi-voluntary” principal reductions. In his paper Clearing the Mortgage Market Through Principal Reduction, he makes the case that negative equity is the reason why the housing market hasn’t bottomed and we need a policy response to it. The solution – make the banks an offer they can’t refuse: Either reduce the principal on your underwater mortgages to home value or we’ll take away your ability to deal with the GSEs or FHA. Since this more or less is a “reduce principal or get out of the business” it isn’t much of a choice. While he mentions that there could be political consequences of these various actions (he looks at involuntary takings as well), he never mentions the possibility that lenders may in fact decide to adjust their risk calculations accordingly, thus drying up credit even more. What good is a new re-negotiated mortgage to the system if the existing homeowner can only sell to cash buyers or buyers that put up 40%? Amazingly, he doesn’t consider the knock-on effects to lender behavior at all. He assumes that things will just continue as before and lenders will write off this intervention as a necessary “one-off” that is really good for them and good for the country. If that is an indication of how liberal policy makers in general think – that the private sector will not react to their policy changes – that explains a lot.

Filed under: Morning Report |

The banks may come to regret not supporting mortgage cramdown in bankruptcy. It’s a better alternative than the current substitutes being floated. At least with bankruptcy, the creditors got a court hearing before a Federal judge.

LikeLike

Regardless of one’s opinion of the specific individuals involved here, this is pretty funny:

http://www.rollingstone.com/politics/blogs/taibblog/more-on-libor-plus-spitzer-takes-on-bartiromo-in-japanese-monster-movie-epic-20120717

LikeLike

“”Well this is not a boat accident. There wasn’t any propeller, there wasn’t any coral reef and it wasn’t Jack the Ripper. It was a shark.”

http://www.cato-at-liberty.org/threat-to-obamacare-is-no-drafting-error/#utm_source=twitterfeed&utm_medium=twitter

LikeLike

“It’s only an island if you look at it from the water.”

LikeLike

Good Ta-Nehisi Coates op-ed in the NYT:

“Leave the Statue, to Remember

By TA-NEHISI COATES

Published: July 17, 2012 ”

LikeLike

jnc:

Maria has been a lifelong shill for Greenberg and of course Spitzer is a ruthless prick. That’s good television.

LikeLike

Jeez, John, what does Chris Fox have against you??? 🙂

LikeLike

obsession is a difficult thing to explain, especially from the object’s point of view.

LikeLike

banned:

obsession is a difficult thing to explain, especially from the object’s point of view.

I know what you mean. I’ve been there too.

LikeLike

John pegged him as someone who moved to a third world country so that he could be part of the one percent there with his level of wealth. Cao dislikes having his hypocrisy so clearly exposed.

LikeLike